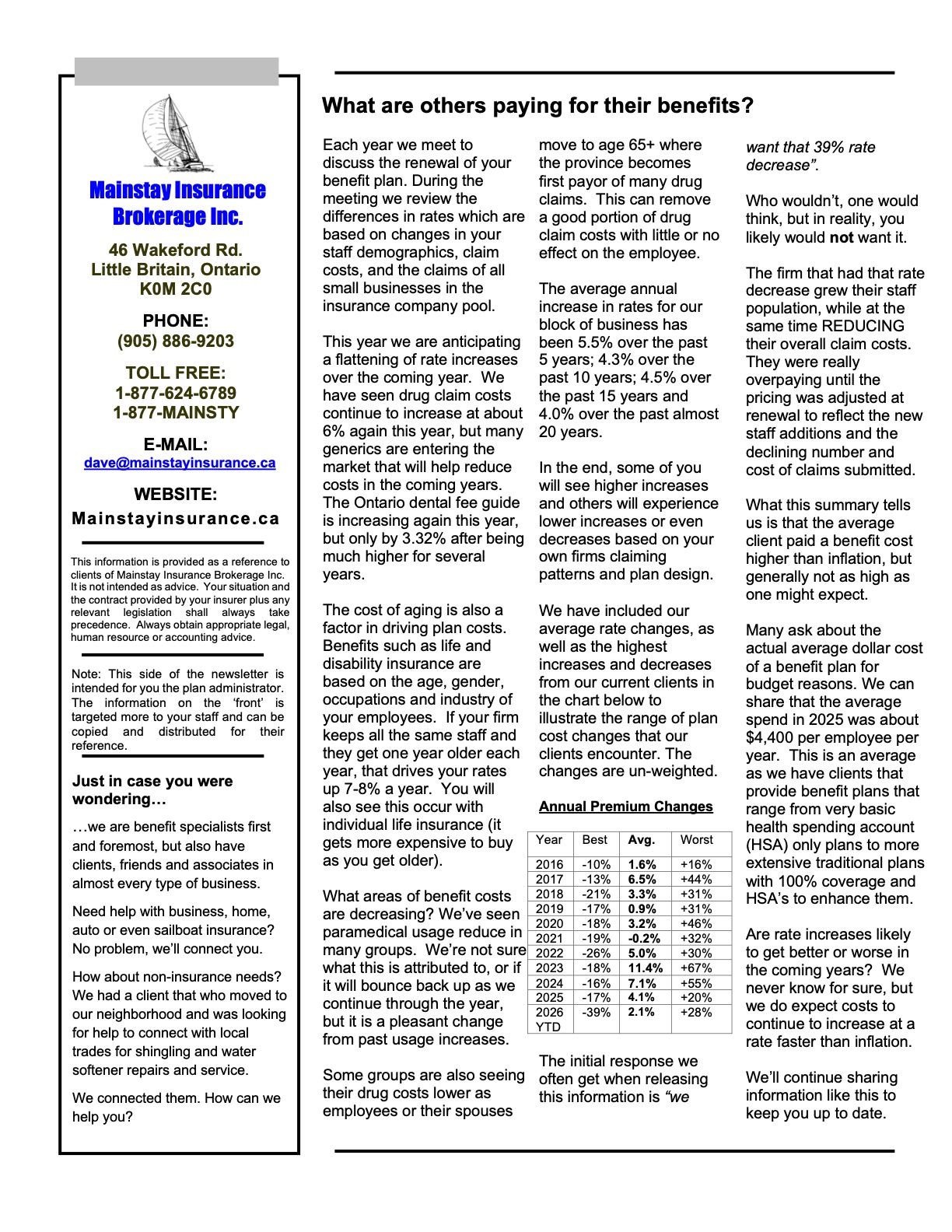

In our April Mainstay News each year, we share our average benefit plan cost increases for our block of business. We also include the past 20+ years of changes on our website. Those numbers reflect our current clients and the results often align or are better than the industry. As an example, a recent article in Benefits & Pension Monitor Magazine had a major national consulting firm say they had “Overall health, including dental, (increases were) around 10 per cent…” which is much more than our bottom line 4% average over 20 years.

The following report share the experiences of a major insurer (not one that we use too often) including the fact that they are very near our clients performance levels.”In 2025, overall per‑capita drug spending increased by 4.0%, marking a slower rate of growth compared to recent years.”

Please read on if you’d like to learn more.

2026 Medavie Blue Cross Drug Trend Report

The drug landscape continues to evolve at a rapid pace, reshaped by new therapies, shifting utilization patterns, and rising expectations for accessible, equitable care. Our Drug Trend Report is designed to help plan sponsors navigate this complexity with confidence. Founded on the strength of our own claims data, the report provides a clear view of emerging trends and the forces affecting drug plan sustainability. Our goal is simple: to equip you with the insights needed to make informed plan decisions so your organization — and your members — are future‑ready.

https://mail.medaviebc.ca/hubfs/2026%20drug%20trend%20report_jul15%20final.pdf